Weekly sustainability insights can now be found by following this link: Sustainability Corner

Weekly Energy Industry Summary

Commodity Fundamentals

Week of July 20, 2026

- Prompt-month natural gas settled at $2.86/MMbtu, down $.05 on Monday, July 20.

- Prompt-month natural gas settled at $2.90/MMbtu, on Monday, July 13.

- Prompt-month natural gas settled at $3.18/MMbtu, on Monday, June 29.

- Prompt-month crude oil (WTI) settled at $84.60/bbl., up $1.37 on Monday, July 20.

- Prompt-month crude oil (WTI) settled at $78.14/bbl., on Monday, July 13.

- Prompt month crude oil (WTI) settled at $70.92/bbl., on Monday, June 29.

Natural Gas Fundamentals - Neutral/Bearish

- A break in the summer heat presents this week in much of the Eastern half of the U.S. with temperatures retreating from the mid 90s to the low 80s. Texas remains very hot. The interior West is very hot. The Southeast is "seasonally hot." The overall effect will be reduced power-generation loads in the 6-10 day period.

- LNG feedgas deliveries have declined modestly (about 1 Bcf per day) as on-going maintenance issues are carried out at the Freeport LNG terminal.

- Production of natural gas has returned to Q1 all-time highs in July. Month-to-date July production averaged 109.7 Bcf per day versus 107 Bcf per day for the same period last year.

- The 2027 natural gas strip-price settled at $3.31/MMbtu, near a three-year low.

- Storage inventories remain on target for a near-record inventory level at the end of October.

- Summary: A break in the summer weather favoring reduced power-generation demand, coupled with near-record gas production, ample storage, and a modest reduction in LNG deliveries overcame summer power-generation demand, pushing near-dated gas futures below $3.

Crude Oil - Bullish

- Three U.S. soldiers were killed in Jordan via an Iranian missile attack at a U.S. airbase over the weekend. Iranian missile and drone attacks were reported in Kuwait and Bahrain on Tuesday. The U.S. has carried out its tenth consecutive day of air attacks on Iranian military targets predominantly near the Persian Gulf.

- Prompt-month (WTI) crude continues to climb settling at $84.60/bbl., up $1.37 yesterday.

- As of this writing crude is trading at $85.62/bbl., up $2.39.

- Over the past seven days 40-45 vessels are reported to have crossed the Strait of Hormuz with 4 vessels having crossed today and no Very Large Crude Carriers have moved through in the past 48 hours, sources say.

Economy - Neutral

- The number of homes going under contract in the U.S. fell 5.4% in June and the pending home sales index dropped to 72.5, The Wall Street Journal reports.

- U.S. jobless claims dropped last week as the number of people who filed for unemployment benefits was 208,000, down 8,000, the Labor Department reported.

- Consumer sentiment improved earlier this month as the University of Michigan's monthly survey rose to 54.4, up from the previous level of 49.5 in June.

- Retail sales grew by 0.2% last month versus the 1% growth recorded in May, the Commerce Department said.

Weather - Neutral/Bearish

- A break in the weather in the Eastern half of the nation brings down the heat from the mid 90s to the lower 80s in the six to ten day forecast.

- Texas remains very hot.

- The Southeast is "seasonal," also-known-as hot and humid.

- The interior West is very hot.

- On a population weighted cooling-degree-day basis, there will be a reduction in power-generation demand in the coming week.

Weekly Natural Gas Report

- Inventories of natural gas in underground storage for the week ending July 10 are 3,024 Bcf; an injection of 41 Bcf was reported for the week ending July 10. Stocks were 21 Bcf lower than this time last year and 181 Bcf above the five-year-average.

Weekly Power Report:

Mid-Atlantic Electric Summary

- The Mid-Atlantic Region’s forward power prices were unchanged over the past week as domestic market fundamentals softened because of cooler temperature forecasts, higher natural gas production and lower LNG send-outs due to maintenance issues. Natural gas prices closed lower for the third straight week, last week, and is continuing that same trend earlier this week. We are seeing cooler trends across the Midwest and East, mostly later this week. The pattern across the Midwest and East looks uneventful this week as the heat remains focused from Texas over into the Western US and Western Canada. A similar pattern is forecast to persist into the first week of August with ridging centered over the Rockies and Plains. The forward electricity prices for the 2027-2031 strips were unchanged over the past week as well as over the past month. The month-to-date, day-ahead settlement price for July thus far in West Hub is $110.31/MWh which is 95% higher than June’s final settlement price average of $56.56/MWh.

- PJM 2028/29 BRA Clears at the Cap and Short - On 7/14, PJM released the results of the 2028/29 Base Residual Auction (BRA). The entire RTO cleared at the collar cap of $325/MW-day, with no Locational Deliverability Area (LDA) price separation. Total RTO committed Unforced Capacity (UCAP) was 6,831 MW below the RTO Reliability Requirement. The auction cleared at an Installed Reserve Margin of 14.4%, or 5.6% below the 20% target. This is the second consecutive auction in which the Reliability Pricing Model cleared short and the third auction clearing at the collar cap. The 2028/29 BRA cleared 138,318 MW of UCAP, an increase of 3,733 MW from the 2027/28 BRA, driven primarily by higher accreditation of existing resources. There was limited new entry compared to the 2027/28 BRA, with 317 MW of new generation and 208 MW of uprates to existing capacity for a total of 524.7 MW of new generation compared to 774.3 MW in the prior BRA. Total Demand Response offered into the auction declined slightly from 7,937.6 MW ICAP to 7,713.7 MW ICAP. Absent the $325/MW-day collar cap, clearing prices would have reached the otherwise tariff-authorized cap of $554.72/MW-day, except in ComEd, which would have cleared at $776.69/MW-day. The higher price in ComEd is driven by the shorter asset life of the reference resource under Illinois' Climate and Equitable Jobs Act and the LDA separation from a lower Capacity Emergency Transfer Limit was largely driven by generation retirements.

Great Lakes Electric Summary

- The Great Lakes Region’s forward power prices trended upward, again, over the past week as domestic market fundamentals softened because of cooler temperature forecasts, higher natural gas production and lower LNG send-outs due to maintenance issues. Natural gas prices closed lower for the third straight week, last week, and is continuing that same trend earlier this week. We are seeing cooler trends across the Midwest and East, mostly later this week. The pattern across those regions looks uneventful this week as the heat remains focused from Texas over into the Western US and Western Canada. A similar pattern is forecast to persist into the first week of August with ridging centered over the Rockies and Plains. The forward electricity prices for the 2027-2031 strips were 2% higher over the past week and the past month. The month-to-date, day-ahead settlement price in COMED for July is $79.23/MWh or is 125% higher than June’s final price, while index pricing in AdHub thus far this month is averaging $85.67/MWh or is 89% higher than June’s final settlement price. In Michigan, the month-to-date, day-ahead settlement price for July is $92.26/MWh or is 112% higher than June’s final price, while in Ameren the month-to-date price is averaging $82.45/MWh or is 122% higher than last month’s average price.

- PJM 2028/29 BRA Clears at the Cap and Short - On 7/14, PJM released the results of the 2028/29 Base Residual Auction (BRA). The entire RTO cleared at the collar cap of $325/MW-day, with no Locational Deliverability Area (LDA) price separation. Total RTO committed Unforced Capacity (UCAP) was 6,831 MW below the RTO Reliability Requirement. The auction cleared at an Installed Reserve Margin of 14.4%, or 5.6% below the 20% target. This is the second consecutive auction in which the Reliability Pricing Model cleared short and the third auction clearing at the collar cap. The 2028/29 BRA cleared 138,318 MW of UCAP, an increase of 3,733 MW from the 2027/28 BRA, driven primarily by higher accreditation of existing resources. There was limited new entry compared to the 2027/28 BRA, with 317 MW of new generation and 208 MW of uprates to existing capacity for a total of 524.7 MW of new generation compared to 774.3 MW in the prior BRA. Total Demand Response offered into the auction declined slightly from 7,937.6 MW ICAP to 7,713.7 MW ICAP. Absent the $325/MW-day collar cap, clearing prices would have reached the otherwise tariff-authorized cap of $554.72/MW-day, except in ComEd, which would have cleared at $776.69/MW-day. The higher price in ComEd is driven by the shorter asset life of the reference resource under Illinois' Climate and Equitable Jobs Act and the LDA separation from a lower Capacity Emergency Transfer Limit was largely driven by generation retirements.

Northeast Energy Summary

- The return of military strikes in the Persian Gulf has both oil and global natural gas higher though not nearly as high as initial post-strike prices back in March. Nonetheless, New England forward markets have elevated on account of those increased risks and the correlation to global natural gas prices due to winter LNG imports. Calendar 2027 and 2028 forwards increased 1.5 and 0.8%, respectively while 2029 and 2030 terms dipped slightly by under 1%. We also saw upward pressure from a PJM forward price rally. Despite bearish natural gas fundamentals, PJM forwards have moved significantly higher (vs. natural gas prices) creating what's known as "heat rate expansion". The pre-July 4 heat wave and expected 90+ degree temps expected on the East Coast this week could be one of the drivers of such buying. Both New England and New York see residual effects from these moves because the PJM market is the most liquid of the power markets and participants in these markets might be experiencing a touch of FOMO as far as upside price risk protection.

- Speaking of upside pricing, the July 1 - 3 heatwave that reached New England did create some momentary price spikes but overall the grid managed through it well without much incident. Day-ahead prices on the evening of July 2 did surpass $900/MWh but was only for a couple of hours with the overall daily average reaching $300/MWh. Additionally, the system did reach a year-to-date peak demand on July 2 between 6 and 7pm at 25,289 MW. This day/hour could be of particular importance in capacity cost allocation for the capacity year June 2027 and May 2028 though a hotter day eliciting a higher peak at any point during the balance of the year could unseat it. Customers that were able to curtail during that time may have been able to capture some future cost avoidance/current Peak Response rebates if the July 2 date/hour holds at the coincident peak for the region.

- On 7/14, Governor Hochul issued Executive Order No. 62 establishing a statewide moratorium on certain data center permitting activities, pausing Department of Environmental Conservation (DEC) approvals for covered projects while the Department of Public Service (DPS) develops a statewide environmental review and related standards. The order applies to data centers consuming 50 MW or more and remains in effect until DPS completes a Final Generic Environmental Impact Statement and findings statement - roughly a one-year review. The order also directs state agencies to develop a Community Investment Framework, evaluate a potential New York Grid Acceleration Fund, convene a Data Center Interconnection Working Group, and review water withdrawal rules. Hochul’s decision comes amid broader review of large-load interconnections, with nearly 12 GW of proposed data center load in the NYISO queue as of May 2026, growing concerns over grid reliability, ratepayer exposure, water demand, and host-community impacts, and months of escalating public and regulatory attention to large loads. On 6/4, both houses of the New York State legislature passed the Responsible Data Center Development Act (S10642/A11560), which would impose a one-year moratorium on DEC approvals for large data centers along with provisions for datacenter load to be served by renewables only. The bill remains unsigned. Earlier this year, the Public Service Commission opened Case 26-E-0045 on 2/12 to advance “Energize NY Development” and reform large-load grid interconnections. The NYISO is also considering revisions to its large-load interconnection study process, while FERC recently issued show cause orders to all six Regional Transmission Organizations, including NYISO, requiring each to justify its large-load interconnection tariff provisions as just and reasonable or propose reforms.

- NYISO’s Q2-2026 Short-Term Assessment of Reliability continues to identify reliability deficiencies in New York City and the Lower Hudson Valley, driven in part by uncertainty around Hydro-Québec’s Champlain Hudson Power Express’s demonstrated capability and the planned retirement of the gas-fired Danskammer units. Because retaining Danskammer would resolve all or part of the Lower Hudson Valley need, NYISO has determined that the units cannot deactivate on 8/1/26, and must remain in service until at least 1/15/27, unless permanent solutions are available sooner, with compensation under an Interim Service Provider rate beginning 8/1/26. The report reinforces NYISO’s concern that aging generation in load-constrained areas remains a material reliability risk as retirements continue to outpace replacement resources. NYISO noted that during the early July 2026 heatwave, generator outages in New York City and the Lower Hudson Valley were two to three times higher than currently planned for, with additional transmission outages placing the grid beyond established planning criteria.

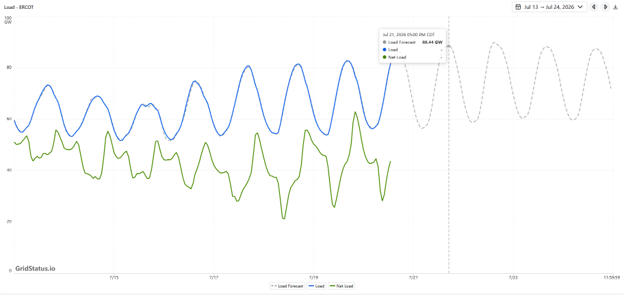

ERCOT Energy Summary

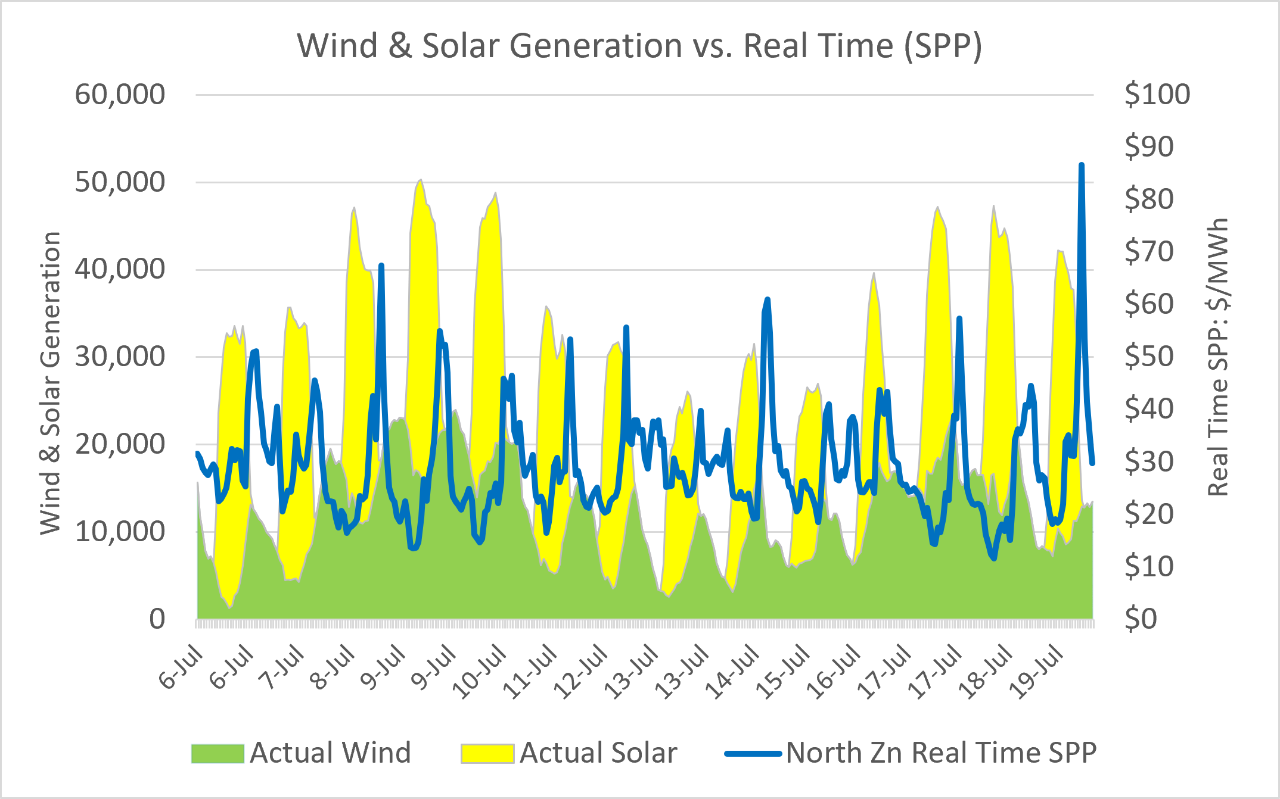

- Summer demand took a pause in the first half of last week with ERCOT load only reaching 65 GW on July 15th before recovering to 80 GW on July 17th and holding through the weekend. Wind dropped early in the week to only 8 GW on a flat average basis along with solar output before rebounding to 16 GW later in the week. Solar followed suit as it recovered to 13 GW but the weekend.

- Looking at the forecast for the next 14 days, Peak heat is forecast to arrive across parts of Texas over the next couple of days, particularly around Dallas where daytime highs are forecast in the mid-100s coupled with low wind generation. Temperatures are forecast to ease a bit towards the balance of this week but remain above normal as wind generation is also forecast to increase. Low 100s are forecast in Dallas this weekend before another spike in temperatures is possible early next week with another round of mid 100s. Elsewhere, above normal temperatures will be common as well with daytime highs in the upper 90s. The above normal pattern is then shown to persists into the first week August, mostly across central and northern Texas while Houston remains closer to normal.

- The one variable at sunset could be wind which is forecasted to only average 7 GW on a flat basis on Wednesday before rebounding later in the week to 15-17 GW. Solar should be consistent at 13 GW this week.

- Complicating the 8-11 day forecast is the emergence of Tropical storm currently situated off the Florida Panhandle. Bertha will very slowly traverse west-northwestward in the coming days as it maneuvers between a ridge situated over the Rockies and a trough in the Northeast. Impacts should be mostly confined along portions of the Gulf Coast where gusty winds, heavy rain at times, and high surf will be seen over the next couple of days. Dry air around coupled with an increase in vertical wind shear should limit Bertha from strengthening further as it approaches Southeast Texas.

ERCOT Load: July 13th - 20th

Source: Grid Status

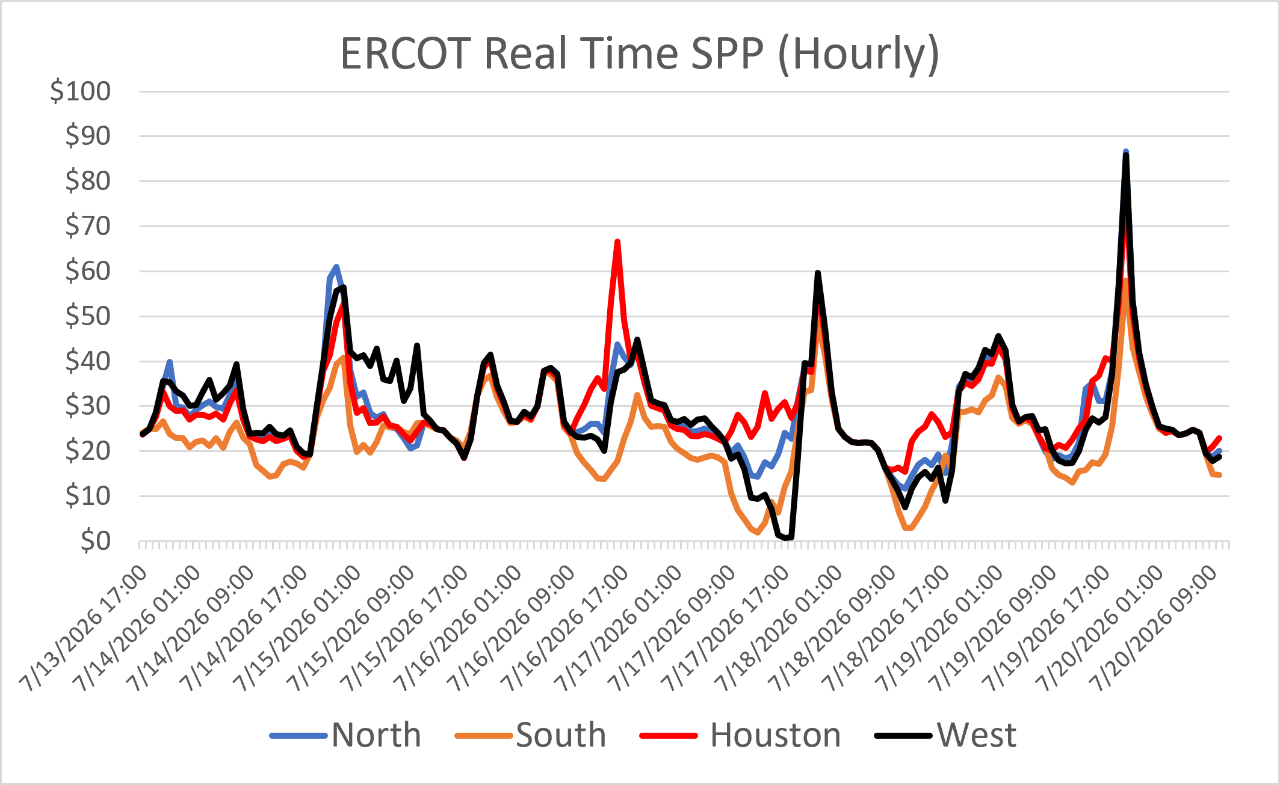

ERCOT Real Time Prices

Source: ERCOT

- Real time prices saw some negative congestion in the South & West zones with real time prices were in the mid $20’s/MWh again as load was overall moderate as mentioned above.

Recent Solar, Wind and Battery Milestones:

- No new records last week. July 4th saw a new battery charging record set of 10,522 MW on July 4th at 9:05 CT, breaking the record set on July 3rd of 9,277 MW. On July 8th ERCOT set a new discharge record for batteries of 11,674 MW breaking the record of 10,372 MW set back on March 13th.

- June 25th saw a new record output for combined renewables of 51,974 MW, the second this week and breaking the previous record of 47,919 MW on May 14th. ERCOT set a new wind record last week at 28,928 MW on May 17th at 11:50 PM CT as winds were strong overnight. The previous maximum wind record of 28,715 MW set on 3/14 at 10:55 pm CT. ERCOT also set a maximum renewables output of 47,919 MW on May 14th at 3:15 pm CT. This was ~900 MW higher than the previous record from last June. The solar record output was set May 2nd at 11:25 am CT with output reaching 33,975 MW/ 4/20. It’s the first new solar record since March 21st at 33,452 MW.

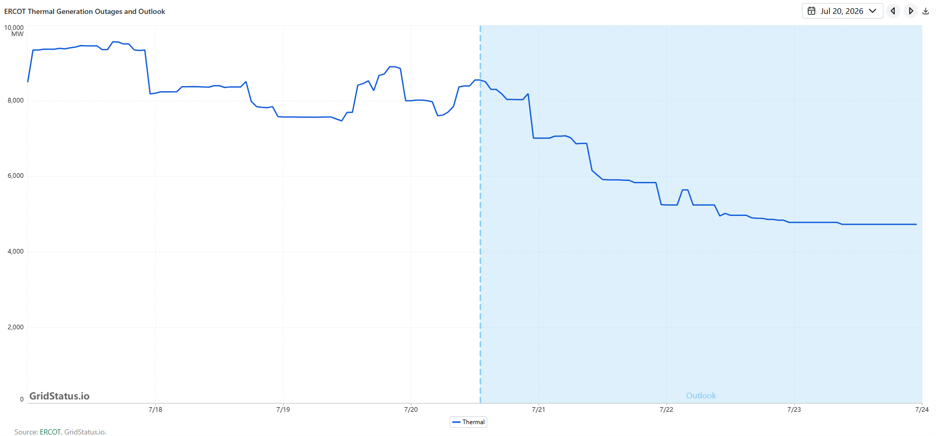

Generator Outages

- Thermal generation outages in ERCOT got down to 8 GW last week and could remain steady in mid-July but with the heat coming this week, ERCOT could use additional generation.

https://www.gridstatus.io/graph/ercot-outages?iso=ercot&outageType=thermal

Source: ERCOT & Grid Status

TX Legislature, PUCT, & ERCOT News:

Texas PUC Approves "Ride-Through" Rules For Data Centers

At its open meeting last Thursday (7/16) the PUCT unanimously approved two new rules (PGRR145 & NPRR1325) under Project No. 54445 titled Review of Protocols Adopted by the Independent Organization. Project No. 54445 would require data centers and crypto miners (+75 mw) to stay stable and connected to the grid through disruptions. This will most likely require batteries and back-up generation.

For some quick background, at its meeting on June 2nd, the ERCOT Board of Directors (Board) recommended the Commission approval of the following two proposed revisions:

• PGRR145, Batch Zero Process for Large Load Interconnections -

• NPRR1325, Related to PGRR145, Batch Zero Process for Large Load Interconnections

On the 16th, PUCT staff walked through a memorandum they wrote in response to request back on June 3rd following the June 2nd meeting to request to comments on ERCOT’s authority to impose the standards approved by the ERCOT Board of Directors (Board) in NOGRR 282, which several Large Loads had since challenged. PUCT staff went through each argument by stakeholders and sided with ERCOT, which wasn’t a surprise. One central argument was PUCT pointed out the contrast between the regulation of the regional electrical network and regulation of consumers that utilize that regional electrical network. They argued that rule (NOGRR 282) was written with the intention that customers would sponsor the interconnection of LCLs, commenters could assume that NOGRR 282 was a regulation of retail customers.

Kenteel Engineering, stated in a June blog on LCL that If LCL’s are allowed to disconnect this could presents a reliability problem in the future as “several hundred — or several thousand — megawatts of computational load all detect the same sag and drop simultaneously, the grid experiences a sudden, large loss of demand.”

The PUCT rule states that “as LCLs increase on the ERCOT System, similar (ride through) events would be expected to increase in magnitude and frequency, leading to frequency instability and other reliability problems absent frequency and voltage ride-through requirements.” Also, as reported by Zero Hedge on the topic, in it’s official comments, ERCOT wrote that LCL loss wasn’t a hypothetical, and ERCOT “has experienced 28 events involving LCL trips of at least 100 MW due to voltage and frequency excursions since the beginning of 2023. This risk will increase exponentially with the significant growth of LCLs expected in the ERCOT Region.”

PUCT/ERCOT Response to Governor Abbott Directive Delayed - In a 6/10 letter to PUC Chairman Thomas Gleeson and ERCOT CEO Pablo Vegas, Governor Abbott directed several actions regarding datacenter protections including a requirement to file a memo to "identify additional actions under their authority to safeguard residential and small business ratepayers and submit a joint memorandum to the Office of the Governor by July 17, 2026." Due to extensive flooding across Central Texas, the Governor has pivoted to emergency flood response and has indicated that he does not expect the PUCT/ERCOT to file responses on the dates requested

CAISO, Desert Southwest and Pacific Northwest Energy Summary

- Changes coming out of World Cup Weekend were mostly in the hotter direction for much of the Western U.S. through the remainder of the month, especially across the interior West. Above to much above normal temperatures will be common from SoCal up through the interior West and into Western Canada. This includes upper 80s later this week in Calgary along with mid-90s in the LA Basin. The monsoon is also shown to ease a bit later this week across the Desert Southwest as above normal temperatures return to Phoenix. The hotter pattern is shown to persist into next week except for California’s coastal population centers where temperatures will yet again skip the excitement and remain closer to normal.

- Little surprise, demand and CAISO power burns came off over the weekend as net load backed away from the highs of last week. Pricing hubs firmed up over the weekend package, PG&E city gate settled up roughly $0.13 from Friday at $2.78/MMBtu, while SoCal’s gate to the city tacked on a nickel to reach $3.42/MMBtu, put the SoCal sunshine premium at $0.65/MMBtu. This upward price pressure is tightly linked to CAISO's net load forecast building back through the front half of the week, leaving the evening ramp and light load hours as the critical swing factors for gas-fired generation while solar output runs near full tilt at midday. On the supply side, regional gas storage inventories continue to diverge, with PG&E's balance grinding lower toward 181.5 Bcf, while SoCalGas’s storage has flattened out around 105.7 Bcf, bringing the combined California gas storage level to 287 Bcf.

- Electricity markets are electric with anticipation for the building heat, CAISO's day ahead auction cleared on Monday significantly higher out of the weekend. Driven by supportive spot gas prices and rising temperatures, NP15's heavy load premium jumped to $47.07/MWh and SP15 rose to $44.73/MWh, representing an approx. $8 increase for both hubs compared to Sunday's settles of $39.51/MWh and $36.99/MWh. This surge flipped the regional spread, putting NP15 back over SP15 with a $2.34 premium, reversing the dominance SP15 held late last week. On the grid operations front, renewable generation showed mixed results as wind gen eased slightly to 3.4 GW from 3.5 GW, while solar output held steady around 8.3 gigs.

- A recent Public Policy Institute of California (PPIC) poll found growing concern about California’s plan to phase out sales of new gasoline-powered vehicles over the next decade. Two-thirds of voters surveyed said they oppose the governors executive order calling for all new passenger cars sold in California to be zero-emission by 2035. While Republicans and independents have long been wary of the mandate, the most notable shift has occurred among Democrats. Half of the Democrats surveyed said they oppose the policy, while 49% support it. That represents a 12-point swing from PPIC’s July 2025 poll, when 55% of Democrats supported the mandate and 44% opposed it. The results highlight the challenges California leaders face as they attempt to accelerate electric-vehicle adoption amid continued opposition from the Trump administration. Democratic gubernatorial candidate Xavier Becerra appears cautious about the mandate. With public support weakening and California’s next governor declining to embrace the current deadline, the future of the 2035 mandate could become a significant political and policy issue over the next 18 months. Also interesting, the majority of Californians are not willing to pay more for electricity generated by renewable sources. Roughly 6 in 10 are opposed with the strongest opposition being located in the Central Valley and Inland Empire (read: areas where AC use blows out in the summer boosting gross kWh of consumption on electricity bills relative to the coastal environs.)

Stay up-to-date on the latest energy news and information:

Coming soon from Constellation Customer Insights: Help us provide you with greater service by completing our online study later this month. For a limited time, eligible customers can choose to accept an incentive for taking the time to provide feedback.

- Energy Market Intel Webinar - Register for our next market update webinar on Wednesday, September 16 at 2 p.m. ET when the CMG team will provide insights on market factors currently affecting energy prices, such as weather, gas storage and production, and domestic and global economic conditions.

- Fortunato & Friends Webcast - Stay tuned for information regarding our next Fortunato & Friends webinar featuring Constellation's Chief Economist and a special guest

- Energy Terms to Know - Learn important power, gas and weather terms.

- Sustainability Assessment - We invite you to complete a brief assessment that helps us learn where your company is in building and/or implementing a sustainability plan. Through these insights, Constellation can customize solutions to meet your needs.

- Subscription Center - Sign up to receive updates on the latest market trends.

Questions? Please reach out to our Commodities Management Group at CMG@constellation.com.